Two advisors with 15 years of experience have each accumulated over $100 million in assets under management (AUM): can they both consider themselves successful? No! Why?

It was with this enigma that advisor Patrice Therriault began his presentation, which immediately followed the panel discussion at the Congrès de l’assurance de personnes 2025 (2025 Life and Health Insurance Conference) held in Montreal, entitled Are Yesterday's Business Practices Still Effective?

Active in financial services since 2016, Patrice Therriault has implemented practices that have allowed him to conduct over 700 new client meetings per year, while reducing his workload to less than 40 hours per week. This success led him to found LabOSF, a company that offers financial advisors optimization services, including coaching based on a comprehensive analysis of their business processes.

In the example of the two advisors he cites, the first has AUM of $105 million and the second $110 million. However, the similarity ends there. “If we’re talking in terms of revenue, they’ve succeeded. If we’re talking in terms of profitability, it’s a different story,” he says.

The first advisor has 6,000 clients and five assistants. Updating client files takes him a considerable amount of time.

The second advisor has only 125 clients, Patrice Therriault continues. “What did he learn? He learned to say ‘no,’” Therriault concludes, explaining the advisor’s small number of clients (see subheading: Planning or when to Say “No”).

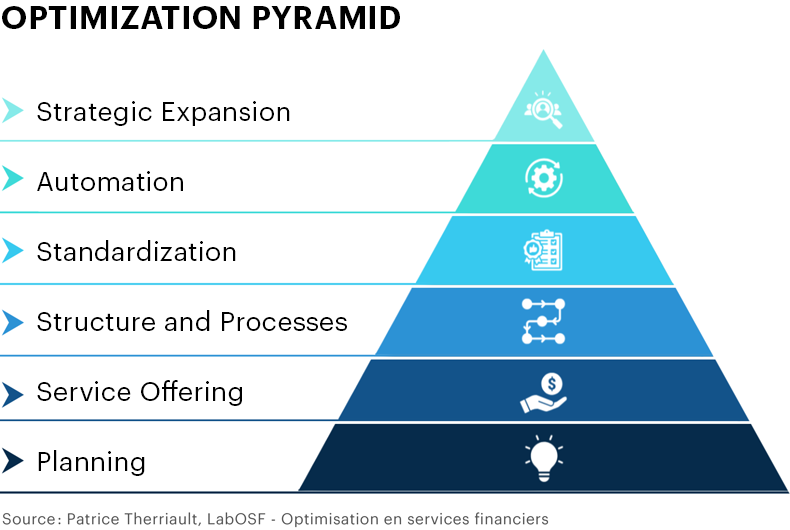

The pyramid of success

Patrice Therriault uses an analogy with Maslow's hierarchy of needs to explain the steps required to achieve a situation like that of a consultant whose thriving practice has only 125 clients. Based on the work of psychologist Abraham Maslow, it was introduced in 1970. It represents a hierarchy of five groups of fundamental needs that humans must fulfill before achieving self-actualization: physiological, safety, belonging/love, esteem, and then self-actualization.

For his part, Therriault prioritizes the six steps to take before reaching what he calls strategic expansion. He uses the Maslow's pyramid analogy to explain the first step of his own: planning. "Ideally, you'll start by eating before buying a cottage," he jokes.

Patrice Therriault demonstrates with an example that you can't skip steps toward strategic expansion, the top of his pyramid. He uses the example of when an advisor hires an assistant. "If you haven't trained the assistant properly and you don't have procedures in place, your return on investment won't be high, because the assistant will cost you a lot in time and money," he says.

Therriault estimates that it takes an average of six months for hiring an assistant to become profitable. According to him, this hire will add greater value to the advisor's business if the advisor has already completed the steps of automating and standardizing their processes.

Planning, or when to say "no"

Patrice Therriault returns to the base of his pyramid to talk about planning. To have 125 clients instead of 6,000, the advisor must, in his opinion, learn to say "no." Why? “When you say no to a client, you increase your value and show them you care. If you say yes to just anyone, you’re not interesting to anyone,” Therriault affirms.

According to him, advisors must know how to choose the right people. But who? He encourages advisors to rate clients from worst to best. The worst, in his opinion, are those “who waste your time.” This is the client who arrives late for an appointment and looks at their phone instead of listening to you; the one who agrees to take out a policy and cancels it the next day; or the one who calls you on Friday evening with endless questions.

Conversely, there is the client who arrives on time and listens to you; who refers you to their family. “That one enriches you. Identify all the criteria that this type of client meets: age, job, hobbies, financial information…” He then suggests dividing clients into two groups based on five criteria.

Segmentation criteria (profitability):

- Assets

- Income

- Age

- Insurance needs

- Investment volume

Qualification Criteria (Respect):

- Arrival time

- Meeting duration

- Interrupts (or not) during the meeting

- Arrives prepared

- Actively listens

Therriault says he will refuse a client willing to invest $5 million, even if they meet all the profitability criteria, if they fail to meet any of the respect criteria.

His approach may differ in the case of a client who does not meet all the profitability criteria, for example, an adult child referred by a parent client. The advisor could then offer them a different deal, in which they might be accepted if they complete certain tasks, such as preparing a budget and committing to saving more to grow their assets.

Entrepreneur or savior?

Patrice Therriault believes that advisors must stop acting as saviors. “Advisors want to advise everyone, say that everyone deserves a chance and has the right to learn about finance.” He tells himself, “I have knowledge, I share it.” Playing the savior? No way! We should think like entrepreneurs,” he underlines.

Thinking like an entrepreneur, according to him, begins by creating a meeting cycle. Leaving the length of a first meeting to chance is out of the question, based on his teachings. “My exploratory meeting is the same for everyone. I want to get to know the person before committing to my entire meeting cycle,” explains Therriault.

Then comes the rest of the cycle: analyzing financial needs, choosing products, subsequent updates, exchanging numerous emails to obtain the necessary documents from clients, and so on. “Over a three-year cycle, my client might have taken 20 hours of my time. Am I prepared to give 20 hours of my time to a client who wants to invest $25 a month?” he asks.

To handle such a case, Therriault urges advisors to ask questions that align with their criteria and follow their process through to the end. For example, if you aim to specialize in clients with higher levels of investable assets, you might say something like: “I don’t accept clients who don’t have at least $100,000 to invest.” This is an effective way to establish credibility and be taken seriously in your market, he adds.

Providing value

How do you refuse the client? By providing value, Patrice Therriault answers his own question. “It might be the son whose father is your client, someone who made an effort to approach you and get to know you, who heard how good you are. They can’t leave empty-handed. You absolutely must give them something. But what? Do like the insurers, who don’t hesitate to refuse, increase premiums, or defer a client,” he suggests.

But what about the client who can only invest $75,000? “Postpone it,” Therriault maintains. “I’ll tell him that I wouldn’t normally serve him, because my business model doesn’t allow it. I’ll ask him to prepare a budget, send me all his information, and do his own analysis. I’ll meet with him afterward.”

He says this will save him the time needed to make the client profitable. A client who arrives late or drags out the meeting will be refused, or perhaps he’ll give them a chance, telling them he only accepts clients willing to invest $200,000 to justify the advisor’s time commitment. According to Patrice Therriault, the foundation of success is to stop improvising, and then to “find your segmentation and qualification criteria,” develop a service offering for each segment, and always provide value.